Home Finance: Routines + Tools for the Bookkeeper at Home. Easy tactics and streamline procedures to reduce the dreaded taboo topic!

First Finance Tip:

Prayer - Ha! Only kidding. Sort of. You guys, when you own your own business, I swear some people think that you’re swimming in gold coins like the cartoon Duck Tales. Please tell me this was someone’s favorite childhood cartoon too!?

Alright, but for real… money has been a stressful situation here in our household before, and no matter what you do for a living, whether you work for someone or own your own business… know you’re not alone. Prayer has sure been something I turn to during stressful times, but let’s get down to the nitty-gritty tips and tricks that you can do to tackle this topic at home:

How I manage them, use certain tools to organize, and tactics to keep my sanity.

Home Finance: Routines + Tools for the Bookkeeper at Home

I mentioned in the video that I really encourage you to read the blog post details below because I link to some of the items I talk about, so you can see what I’m talking about and referring to.

So if you aren’t able to watch the video now, that’s a-ok; you can see details below. But I totally encourage you to come back and watch it when you get time, because sometimes hearing it sinks in more than reading it.

1. Quickbooks

Back when I worked in my husband’s office as a bookkeeper, I started using Quickbooks. I was terrified and so intimidated by it - until I started using it. It is incredibly user-friendly, and I picked it up super quick.

When I came back home full-time, I knew I wanted to continue using Quickbooks for our home finances. This way, I can track expenses easily, and believe it or not… using Quickbooks makes finances so much easier. I have mine set up to where it syncs with my bank and my credit cards, so that’s less data entry that I have to do. Plus, I use the online version so I can track/use it if I’m about and about if I need to! It’s crazy good to be able to keep track of where and how you’re spending money and come tax time, your accountant may just love you.

I have the Simple Start plan, and you get it free for 30 days! You can sign up for it here:

Get Quickbooks

I also use Quickbooks for my business (this here blog), and it’s so nice to be able to track my income/expenses each month and see how much I make and bring in each month/year.

2. Pick a Day Each Week

I’ve chatted about theme days before on Creating Your Happy, and finance falls into one of my theme days.

I know each week on Tuesday (for example), that THAT’S the day I work in my finances. So each week, I know when Tuesday rolls around, it’s go-time. I log in to my Quickbooks, grab my “bills to be paid” folder, my wallet, and I get to work.

This can routine can work if you get a paycheck once a week, every two weeks, randomly in bigger chunks, or however you make an income. For example:

Weekly/Bi-Weekly Paycheck:

If you get paid every two weeks on Friday, perhaps setting your “finance day,” to every Saturday morning would be a good fit for you. On the Fridays where you get a paycheck, you know that the next morning is when you sit down and pay the bills. But on the Saturday morning after a Friday that you do not get paid… YOU STILL sit down and work on finance. This could look like:

- Updating your checkbook/Quickbooks

- Gathering up bills and taking a mental note of what’s on the horizon

- Following up on a bill that you’ve been meaning to call and ask a question about

So even though you may not physically be paying bills on your “off” week, still sitting down, updating and checking in, can make a HUGE difference.

Things won’t catch you off-guard as much, you may not forget about that “one” bill that you’ve been meaning to check in to, etc.

Self Owned Business/Commission Income:

If you own your own business or work off of commission, this routine can be so beneficial. Checking in once a week, whether you have the funds yet or not… can be a huge help.

Updating transactions weekly can really help avoid the dreaded bank reconciliation time, or “Crap, how much do I REALLY have in the account” moments, by organizing and updating it in small chunks. No one wants to sit in front of a checkbook for 5 hours on a Saturday updating 3 months of transactions, do they?

Plus, when you still check in weekly, whether you’ve received your commission or payout from a project yet or not… you’ll most likely avoid the “Oh crap, I thought I was going to have WAY more than that left-over after I paid bills…” when you finally got paid.

Weekly & Bi-Weekly

So, like with the weekly/bi-weekly paycheck people above, your “off weeks” could look something like this when waiting for the “big” check to come in:

• Update your checkbook/Quickbooks

• Gather up bills and take a mental note of what’s on the horizon

• Follow up on a bill that you’ve been meaning to call and ask a question about

Your finance day can be chosen by you. What day/time do you REALLY see yourself working on this for a few minutes each week?

Don’t set yourself up for failure before you even start. Then, once you determine that day… stick to it. You’d be surprised how much better your days/weeks can become if you just sit down and tackle it in small chunks, instead of assuming/ignoring your finances.

Don’t Ignore It

With finance being so taboo in some homes, we tend to ignore it until we have to deal with it. Which this can cause so much anxiety, fear, and overall misery in our day to day when something triggers a thought relating to it. Not to mention the unhealthy spending habits that some can make when they assume they had enough money to buy that new hot tub they’ve wanted.

3. Mobile & Automatic Deposits

Yes, I know this may not be an “ah-ha” moment for some of you. But for those of you who haven’t given it a chance, just hear me out. I fought this so hard for so long too. It was new and I didn’t trust it. But the moment I tried it for the first time with a small $8.00 check (because what do I have to lose?) was so refreshing to know that I didn’t have to pack the kids up or remember to stop by while out running errands to make the deposit.

Give that mobile deposit (if your bank offers it) a chance. The time that you save waiting in line, packing the kids in the car, driving across town, can be a game-changer.

4. Same Online Login for Accounts

I mention in the video above that I’m NO Dave Ramsey. And if he watched this, he may slap my hand. For those who really lack in the financial management and self-control area… this may not be a good tip for you.

But for those of you who do have some self-control, this may be a helpful tip. I keep at least two of my accounts under the same bank login. Why? Because when I forget or need something at the last minute (on the weekend, evening, whenever) I’m able to go into my bank login and make a transfer of funds from one account to the other. It automatically hits and I’m able to use the funds right away.

This could vary from bank to bank, but this practice has come in super handy for me.

Example: It’s Sunday morning and your refrigerator just went out. Your emergency money is in your savings account, but you need it in your checking PRONTO so you can use the debit card to buy a new one. Tomorrow is a holiday and the banks are closed. It will be Tuesday before you can get to the bank and withdraw your emergency money.

If the two accounts that you have under your bank login are a savings account (that you only touch during emergencies) and a checking account (that you use to pay your daily/monthly bills) or if your emergency checking and your regular checking were on the same bank login, you could (depending on your bank) just transfer to the money to the checking account and head to Lowe’s to snag a new fridge.

Less stress + less work = sanity.

5. Determine Who Gets What Debit Card

The moment my husband looked at me and said,

“How about I get rid of this debit card, so you’re the only one that has it, and then I’ll have my own? That way, you’ll always know what’s coming out when and there won’t be any surprises?”

…changed our marriage-financial relationship. I no longer go day to day thinking, “Well what if he used the debit card today for something big that I didn’t plan on him getting?”

This can look different in so many households, and I get it. But if you find yourself constantly arguing, getting upset because he/she didn’t bring that receipt back to you, or they forgot to tell you about that big purchase he/she made that just made a check that you made out and mailed, bounce… I really encourage you to come to an agreement on who has what debit card.

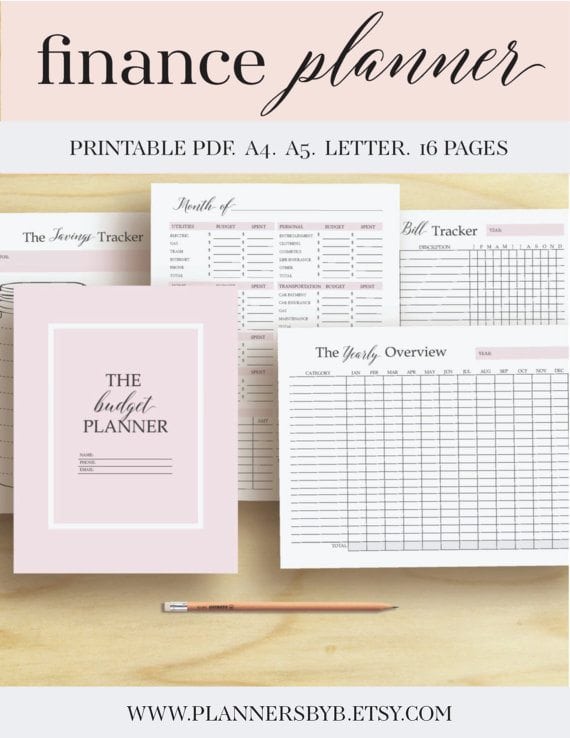

6. Finance Printables

Last, if you’re a pen and paper kind of person, then you just may LOVE the finance printables that I use and fell in love with. I’ve mentioned these in a blog post before: 7 Organization Ideas & Tips to Stay Organized, and I thought they were worth mentioning again.

I love being able to have an overview of what’s coming up, and there’s just something about being able to handwrite it all out to make it “stick” in my brain. So if you’re wired like me, you may find these super helpful too. You can get them here:

Finance Printables

Or, if you have debt to payoff, this debt tracker free printable will be so helpful too!

I so hope you found these home finance tips helpful and found something that may take some stress off of a sometimes stressful topic in your house!

For more tips like this, you’ll LOVE my post on How to Make Your Desk Work More Productive!

Thank you so much for coming by. I’d love it if you’d drop a note below to say hey, and tell me what you use to help with your finances at home!

Evelyn says

How do you trust using on-line products like Quickbooks especially when sinc’d to your bank and debit cards?

Jessica says

Hi Evelyn! I see how it can be worrisome for sure if you connect it to your bank, but I’m hoping with Quickbooks being such a large company, that they have the safety measures in place for it. (Which, even if so, I’m sure there’s always a chance of something happening!) But I love Quickbooks’ features even without the sync!